Rupiah Translucent Rp. 16,240, Two Monetary Policy Options Open

An increase in the benchmark interest rate of 25 bps as an effort to stabilize the exchange rate actually has the potential to depreciate the rupiah.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

Officers serve foreign exchange transactions at PT Valuta Artha Mas in Jakarta, Tuesday (16/4/2024). The exchange rate of the rupiah was recorded to weaken, breaking through the level of Rp 16,200 per US dollar after the 2024 Eid holiday.

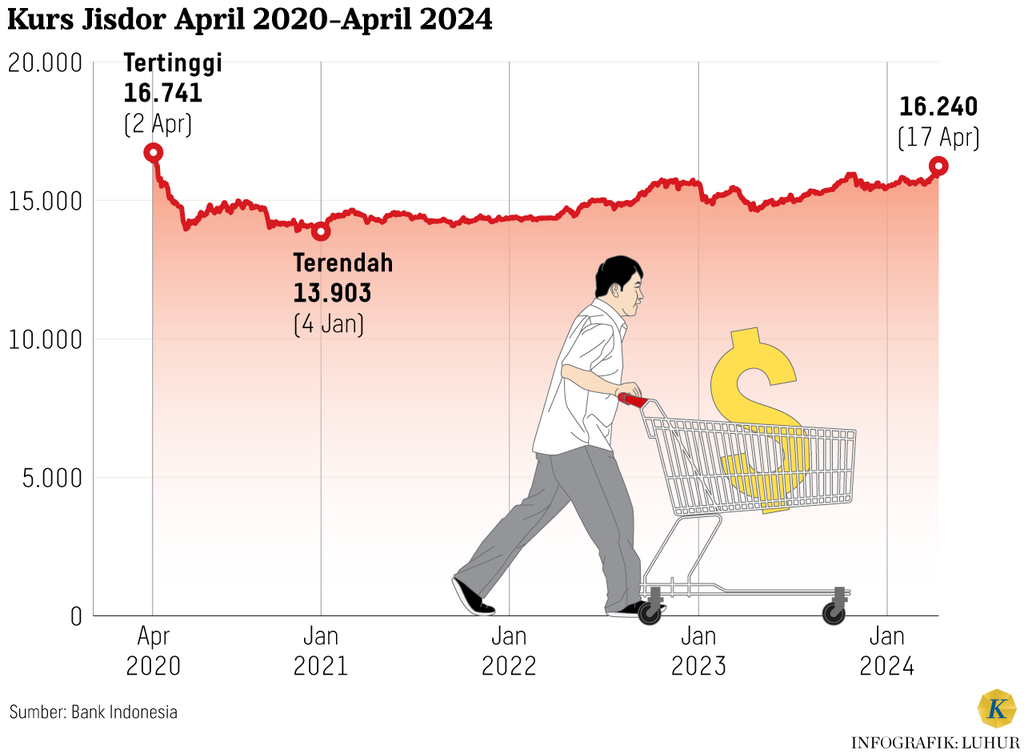

JAKARTA, KOMPAS — Referring to Jakarta Inter Spot Dollar (Jisdor) data, the rupiah exchange rate in trading Wednesday (17/4/2024) closed at IDR 16,240 US dollars or weakened 0.39 percent compared to previous closures. The weakening of the rupiah has reached its deepest point during the 2023 period and is approaching the peak of depreciation in the 2020 period.

The weakening of the rupiah opens up two possible scenarios monetary policy that will be pursued by the central bank. To restore the rupiah above IDR 16,000 per US dollar, it would require at least market intervention around 1 billion US dollars from foreign exchange reserves.

Head of Monetary Management Department of Bank Indonesia (BI) Edi Susiato stated that the current weakening of the rupiah is still caused by global sentiment. This sentiment is due to the release of fundamental data from the United States indicating that the US economy is still resilient, thus lowering expectations for a decrease in benchmark interest rates, as well as the escalation of conflicts in the Middle East.

As a result, the US dollar index strengthened sharply against other currencies, including the rupiah, in the past week. Meanwhile, domestically, there is still an adjustment period after the long holiday, causing the exchange rate to significantly weaken as soon as the market opens.

"BI certainly takes steps, such as ensuring it is in the market to continue to monitor or maintain foreign currency supply-demand balance, encouraging foreign inflow by increasing the attractiveness of rupiah assets and reducing "hedging costs, as well as building coordination with relevant stakeholders, including the government, banking and Pertamina," he said when contacted. Pertamina in this case is the provider of fuel oil in the country.

Senior Economist of PT Samuel Sekuritas Indonesia, Fithra Faisal Hastiadi, explains that there are two policy options that Bank Indonesia (BI) can take to stabilize the exchange rate. Firstly, BI can pursue a benchmark interest rate policy with the hope of triggering rupiah appreciation.

"Based on our simulations, when interest rates are raised, there is actually potential for depreciation. When there is a 25 basis point increase in interest rates, there will be a depreciation of around 50 basis points. This is in the short-term effect. In the long-term, the rupiah will appreciate over a period of more than 2 weeks or 1 month," he said when contacted from Jakarta.

However, once the trend of depreciation begins, the exchange rate will tend to continue weakening due to market pressures and expectation factors. Learning from the depreciation of the Japanese yen when the Bank of Japan (BOJ) raised its benchmark interest rate in the last 17 years, market reactions to expectations of interest rate hikes will tend to be difficult to control and therefore need to be anticipated.

Also read: Rupiah Falls 303 Points, Impact on Industrial Competitiveness is a Concern

Therefore, another option that can be taken by the central bank to stabilize the exchange rate is through market intervention policies. According to Fithra, this effort will be taken at least until June 2024 or wait and see by relying on foreign exchange reserves.

"Based on simulations, with 500 million US dollars, the minimum it could do is bring the rupiah from Rp 16,200 to the level of Rp 16,000. If we want it to be stronger, 1 billion US dollars could bring back the rupiah to the level of 15,900. This can be done for 3 months until June 2024," said Fithra, who is also a lecturer at the Faculty of Economics and Business at the University of Indonesia.

An increase in interest rates of 25 bps can immediately cause the market to react negatively.

As of the end of March 2024, Indonesia's foreign exchange reserves position recorded 140.4 billion US dollars, which is a decrease compared to the previous month of 144.0 billion US dollars. The foreign exchange reserves are equivalent to financing 6.4 months of imports or 6.2 months of imports plus government foreign debt payments. In other words, the foreign exchange reserves are still above the international adequacy standard of around 3 months of imports.

Although still sufficient, the use of foreign exchange reserves of 1 billion US dollars for market intervention for a month needs to be done in a measured manner. At least, market intervention relying on foreign exchange reserves can be effectively carried out for three months.

This is considering the market may react negatively again when there is an announcement of a reserve decrease of up to 130 billion US dollars after the intervention. In other words, intervention policies need to be carried out while optimizing the absorption of export earnings (DHE). According to Fithra's analysis, there is still potential for DHE absorption of around 5-8 billion US dollars.

Also read: Weakening Rupiah Potentially Triggers Price Surge, Entrepreneurs Hope for Intervention

Interest rate policy

If the conflict in the Middle East escalates and escalates, interest rate policy cannot be avoided. This takes into account the strengthening of the US dollar which has an impact on depreciation of the rupiah and the potential for inflation of imported goods (imported inflation).

From the simulation results conducted by Fithra, a 25 bps increase in interest rates can immediately cause a negative market reaction. Conversely, a 50 bps increase in interest rates will tend to delay market reactions, even though it has a significant shock effect.

Employees estimated the value of gold jewelry sold by visitors at Bintang Timur Gold Shop in Kebayoran Lama Market, South Jakarta, on Wednesday (17/4/2024). Traders admitted that some visitors sold their gold jewelry after the post-Eid al-Fitr season.

On a separate note, the Head Economist of PT Bank Central Asia Tbk (BCA), David Sumual, has stated that raising interest rates is one of the options during inflationary pressures. The increase in inflation is caused, among others, by the weakening of the rupiah and the surge in global oil prices.

"Bank Indonesia (BI) can change its monetary policy direction if inflation is impacted. However, so far, inflation is still relatively under control, only affected by seasonal spikes in food prices," said David when contacted.

Until now, the impact of the spreading heat of geopolitical tensions in the Middle East on oil prices and the US dollar index cannot yet be predicted. Nevertheless, the government needs to adjust domestic policies, including expectations regarding changes in the price of fuel, which can affect inflation and the economic situation.

BI could change the direction of monetary policy if inflation is affected.

According to David, the increase in BI's benchmark interest rate is likely to have derivative effects on loan interest rates. However, this is still uncertain given that consumer credit interest rates have actually tended to decrease amid the trend of high interest rates over the past year.

"This reference interest rate policy is more directed at preventing even larger outflows from occurring. We still need portfolio capital flows because there is a tendency for our current account to be in deficit. "Therefore, policies are needed to keep the rupiah attractive and prevent investors from leaving the domestic market," he said.

The Governor of Bank Indonesia, Perry Warjiyo, answered questions from journalists during the press conference following the Board of Governors Meeting at Bank Indonesia in Jakarta, on Wednesday (20/3/2024).

Going deeper and deeper

In addition to the depreciation of the rupiah against the US dollar, the Composite Stock Price Index (IHSG) closed in the red or weakened by 0.47 percent at 7,130.84 bps on Wednesday (17/4/2024) after briefly strengthening in the morning. The current condition of the domestic financial market is still colored by the sentiment of escalating geopolitical tensions in the Middle East.

At the opening of the first trading session until 09.20, the JCI had strengthened 0.95 percent at the level of 7,232.74, an increase from the initial position at the opening of trading at the level of 7,164.807. Meanwhile, on Tuesday (18/4), IHSG fell 1.68 percent or fell 122,075 basis points to 7,164,807 after opening trading at 7,286.

At the close of Wednesday, there was a selling action (net sell) by foreign investors amounting to IDR 470.67 billion. Thus, the value of foreign investment has left the domestic stock market amounting to IDR 2.86 trillion over the past month.

Index movements were monitored from monitors at the Indonesia Stock Exchange in Jakarta, Tuesday (16/4/2024).

Based on data as of April 4, 2024, non-residents recorded a net purchase of Rp 8.25 trillion in the domestic financial market. The portfolio investment consists of a net foreign sell of Rp 34.75 trillion in the State Securities market, a net buy of Rp 23.95 trillion in the stock market, and a net buy of Rp 19.05 trillion in the Indonesian Bank Securities market.

Head of the Literacy, Financial Inclusion and Communication Department of the Financial Services Authority (OJK) Aman Santosa said that the value of share ownership of investors from the Middle East was recorded at IDR 65.73 trillion or around 2 percent of the total value of share ownership of non-resident investors. Ownership of financial services institutions (controllers) by investors in the Middle East is recorded only in banking with an asset share of 0.1 percent of total banking assets.

"However, the OJK will continue to monitor market risk developments in Financial Services Institutions and pay close attention to financing to sectors that have high exposure to conflict in the Middle East, including paying close attention to the condition of individual financial services institutions," he said in a statement. official.

The Financial Services Authority (OJK) also assesses that the stability of the national financial services sector remains well-maintained, supported by strong capitalization, adequate liquidity, and managed risk profiles that are capable of facing the increase in global geopolitical tensions. Meanwhile, the fundamentals of the Indonesian economy are still well-maintained, as evidenced by the maintenance of growth in the range of 5 percent, inflation within the range of the Bank Indonesia's target, a still-surplus trade balance, adequate foreign exchange reserves, and available fiscal space.

In February 2024, the direct exposure of the Financial Services Authority to the Middle East region is relatively limited. Domestic banks only hold securities issued by the Middle East worth Rp 1.3 trillion, or 0.06 percent of the total securities held by banks, while insurance and financing companies do not have any securities issued by the Middle East.

Also read: After falling after the Eid holiday, JCI opened stronger