Himbara's Net Profit Growth Returns to Normal

Three of the four banks recorded net profit growth that was much lower than in the first quarter of 2023.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

Officers from Bank BTN provide currency exchange services at the integrated mobile cash service organized by Bank Indonesia along with other banks at Istora Senayan, Jakarta, on Thursday (28/3/2024).

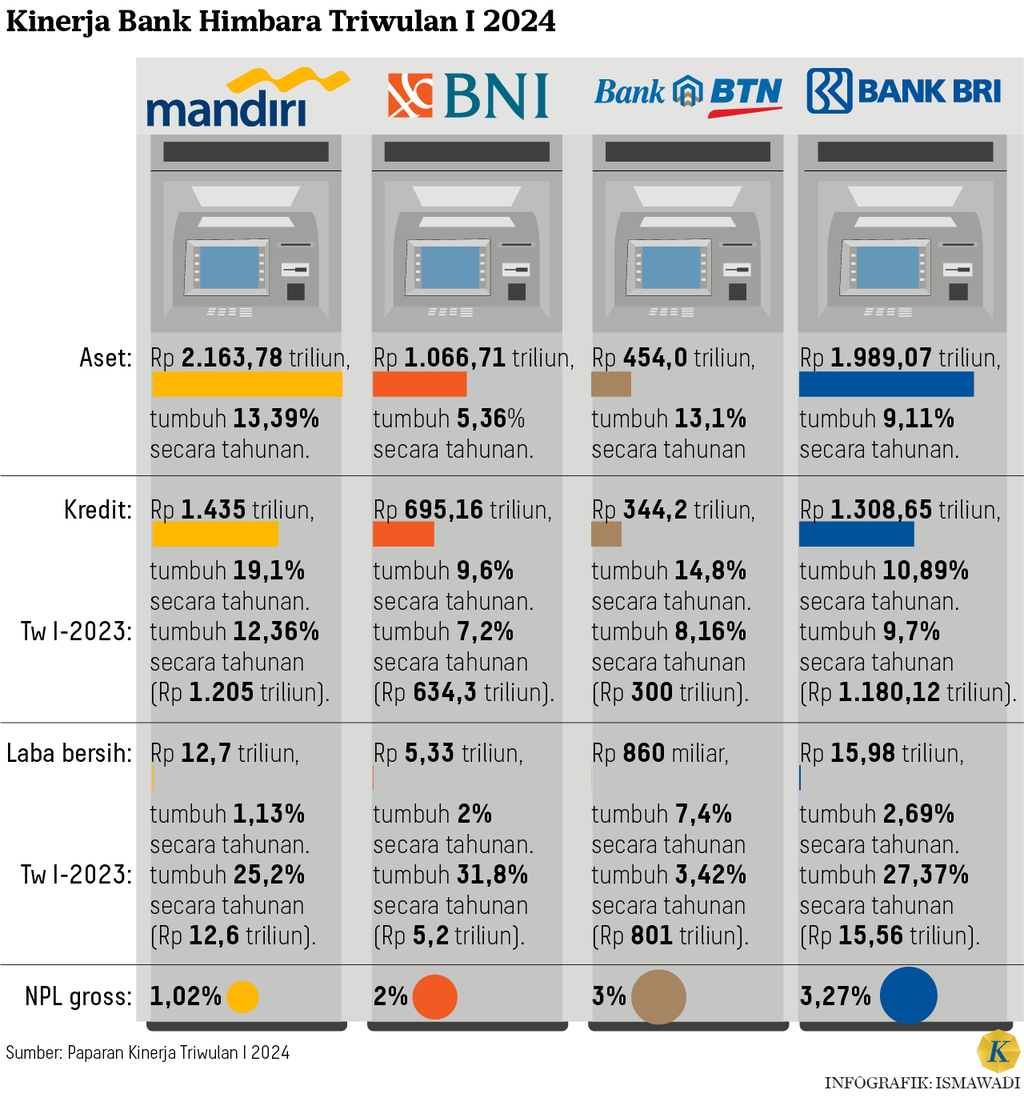

JAKARTA, KOMPAS – The growth of net profit of the Association of State-Owned Banks or Himbara in the first quarter of 2024 was lower than last year. This shows that the formation of loss reserves returned to normal along with the end of the credit restructuring policy. In 2024, Himbara's net profit and credit distribution are expected to grow moderately due to the interest rate policy.

Himbara recently released its performance report for the first quarter of 2024. They are PT Bank Mandiri (Persero) Tbk, PT Bank Negara Indonesia (Persero) Tbk or BNI, PT Bank Tabungan Negara (Persero) Tbk or BTN, as well as PT Bank Rakyat Indonesia (Persero) Tbk or BRI.

Overall, Himbara's credit distribution in the first quarter of 2024 was recorded at around IDR 3,783.01 trillion or grew 13.96 percent annually. This is higher than the average credit distribution by the banking industry which grew 12.4 percent annually.

Also read: Banking Credit Can Continue to Grow 10-12 Percent

However, three out of four banks recorded lower growth in net profits compared to the first quarter of 2023, which managed to reach double digits. In the first quarter of 2024, the net profits of the three banks only grew around 1-3 percent.

Senior Economist and Associate Faculty of the Indonesian Banking Development Institute, Ryan Kiryanto, said on Saturday (5/4/2024) that the slowing growth of net profits could be a banking effort to prepare for the end of the Covid-19 credit restructuring policy. The policy ends on March 31, 2024.

"During restructuring, banks' CKPN (allowance for impairment losses) becomes cheap. Before the restructuring ended, the banks had already acted as if the policy had ended so that CKPN formation returned to normal. "In other words, they are back to normal," he said when contacted from Jakarta.

The Financial Services Authority (OJK) has set a policy of credit restructuring for sectors affected by the Covid-19 pandemic, also known as a relief scheme for debt repayment. This is regulated in Financial Services Authority Regulation (POJK) Number 48/POJK.03/2020 Year 2020 concerning Amendments to POJK Number 11/POJK.03/2020 regarding National Economic Stimulus as Countercyclical Policy on the Impact of the Spread of Corona Virus Disease 2019.

This policy provides relief for debtors in the form of reducing interest rates, extending deadlines, reducing principal arrears, reducing interest arrears, increasing credit facilities, as well as converting financing into temporary capital participation. On the other hand, banks do not record these debtors in collectibility 3-5 or non-performing loans (NPL).

Rather than raising the credit interest rate which burdens debtors in fulfilling their obligations and results in new non-performing loans, it is better not to increase the credit interest rate despite the need to adjust the deposit interest rate with the consequence of reducing net interest income.

Meaning, the burden for forming CKPN towards loans that have received restructuring is reduced. In other words, the profit obtained by the bank will not be eroded to form CKPN.

Ryan believes that despite lower net profit growth compared to the previous year, Himbara can be said to have prepared themselves well in advance before the OJK stimulus policy ended. This is reflected in their reserve ratio, which averages above 200 percent.

Also read: BI Interest Rates Rise, Bank Credit Distribution Risks Slowing

Maintain credit quality

Not provided due to violation of Zero-shot translation capabilities.

Ryan explained that the increase in the BI rate does not automatically make banks immediately raise their savings or loan interest rates. Bank decisions to raise interest rates are more influenced by liquidity conditions of each individual bank.

"Rather than raising loan interest rates, which would burden debtors in fulfilling their obligations and lead to new non-performing loans, it is better not to increase loan interest rates even though it may require adjusting deposit interest rates with the consequence of reducing net interest income," he said.

This option is taken to maintain the credit quality so that the bank does not have to form a large Non-Performing Loan (NPL) ratio. This is in view of the fact that the increase in loan interest rates will affect the ability of debtors to fulfill their obligations.

"Increasing credit interest rates will result in NPLs and CKPN so that net profits will be further eroded," said Ryan.

Deputy Minister of State-Owned Enterprises Kartiko Wirjoatmodjo, accompanied by the President Director of PT PP (Persero) Tbk Nover Arsjad and the President Director of PT Hutama Karya (Persero) Budi Haryo, explained the concept of the State Capital for the future generation at Sepinggan International Airport, Balikpapan, on Saturday (24/12/2022).

Previously, Deputy Minister of State-Owned Enterprises (BUMN) Kartiko Wirjoatmodjo said that managing liquidity and the dynamics of interest rate policies would be quite challenging until the end of 2024. This is not unrelated to the global macroeconomic conditions that are still shrouded in uncertainty.

"This will certainly make banks more cautious. Banks will tend to grow in the range of 10 years plus or minus a little more moderately. Therefore, the growth of bank profits and credit growth will tend to be more moderate," he said when giving a speech at the Bisnis Indonesia BUMN Forum 2024 in a hybrid format, on Tuesday (30/4/2024).

Based on OJK's data, bank credit distribution in March 2024 reached Rp 7.244 trillion or grew by 12.4 percent annually. On the other hand, credit quality remains maintained with NPL net and gross ratios of 0.77 percent and 2.25 percent respectively.

Main Director of Bank Mandiri Darmawan said, in facing fluctuating economic dynamics, Bank Mandiri continues to prioritize the principle of prudence. This is reflected in the gross NPL of bank only which was maintained to the level of 1.02 percent as of March 2024 or down from the same period last year of 1.7 percent.

Officials from Bank Indonesia are serving the public who are exchanging money at the integrated mobile cash service provided by Bank Indonesia and banks, at Istora Senayan, Jakarta, on Thursday (28/3/2024).

Apart from that, Bank Mandiri is conservative in determining credit reserves as reflected in the bank only coverage ratio which is at the level of 368 percent. The improvement in credit quality is also reflected in the cost of credit (CoC) being maintained at a low level of 0.99 percent.

"In encouraging credit distribution, we will continue the strategy we have implemented over the last few years, namely strengthening Bank Mandiri's core competence in the wholesale segment and increasing growth in the retail segment. with an ecosystem-based value chain approach and a focus on leading sectors in Indonesia," said Darmawan in his official statement, Tuesday (30/4/2024).

Meanwhile, BNI's gross NPL ratio in the first quarter of 2024 was recorded at 2 percent or down from the same period the previous year of 2.8 percent. This was followed by a reduction in credit costs to 1 percent.

Also read: Government Beware of Impact of Global Uncertainty

BNI's President Director, Royke Tumilaar, stated that improving asset quality is expected to encourage sustained intermediation amidst global geopolitical challenges, inflation pressures, and interest rates. In addition, the company continues the ongoing corporate transformation that has been running for three years to deliver strong and healthy profitability levels in the long term.

"The Fundamental BNI is growing stronger and healthier thanks to the transformation program that has become our big step to continue to grow, develop, and adapt to challenges at the national and global level," said Royke.