The digital transformation should be further pushed to increase financial inclusion, which could in turn strengthen economic recovery efforts.

By

ENNY SRI HARTATI

·6 minutes read

KOMPAS/TOTOK WIJAYANTO

Enny Sri Hartati

Before the Covid-19 pandemic hit Indonesia, the government intensively campaigned the importance of Industry 4.0. Almost all ministries and agencies have initiated programs and allocated a budget for the digital technology adoption. However, various digital programs, such as e-learning, e-forms, e-documents, e-procurement, e-commerce, e-budgeting, and other similar network services, seem to have gone nowhere.

Since the emergence of Covid-19, without a structured and systematic program, the public has been "forced" to adapt to go digital. During the pandemic, the number of internet users is estimated to reach 175.4 million people or around 64 percent of the total population in Indonesia. The number of the social media users alone is estimated to reach 160 million people.

There has been a very fast and drastic increase in the use of digital technology as almost all educational activities have to be held online or virtually. Economic activities are no exception as they have to be shifted to digital in order to adapt to the Covid-19 protocol. It is not an exaggeration to say that the pandemic has practically accelerated the digital technology revolution.

Such an opportunity should be optimized to mitigate the impact of the Covid-19 pandemic on the economy. At least it can be used to minimize polemic, whether we should prioritize health or economy. The use of digital technology can increase efficiency because production costs could be reduced by between 12 to 15 percent. Moreover, the digital technology not only boosts online transactions but also improve financial literacy or access to the financial sector. That said, Indonesia\'s digital economic potential is the greatest in ASEAN.

It is not impossible because the Indonesian population is the largest in ASEAN. In a relatively a short time, public literacy on financial services has increased rapidly. The 2019 National Financial Literacy Survey (SNLIK) shows that the financial inclusion index reaches 76.19 percent. It means that the public access to financial services and products or "financial literacy" has increased significantly.

Unfortunately, the survey conducted by the Financial Services Authority (OJK) shows that the level of public understanding on financial products is 38.03 percent. The use of financial products for productive economic activities is, for example, still limited. In fact, there is a significant improvement in the financial inclusion but more due to the increase in the number of savings accounts, especially after the government changed the distribution of the rice assistance for the poor (Raskin) from cash to bank transfers.

Distribution of social assistance package stage 4 from the Provincial Government of DKI Jakarta to residents affected by Covid-19 at RW 06, Cipulir Sub-District, Kebayoran Lama, South Jakarta, Tuesday (30/6/2020)

In fact, Bank Indonesia and the OJK made a breakthrough in financial services several years ago with the launch of branchless banking and the presence of bank agents.

Initially, financial inclusion through the launch of branchless banking was intended not only to facilitate the distribution of government assistance, but also to increase the access of the poor to banking services and products. At least, the database on the profile of the poor has been on the banks’ radar so that their presence can be recognized, enabling them to gain access to financial products such credits especially for ultra-micro business. The use of financial products for productive economic activities is still limited.

Transparent and accountable

The distribution of the social assistance through the banking system will certainly more transparent and accountable. The data of recipients cannot be manipulated and can easily be integrated with various social protection program schemes. At least it can reduce the loophole for moral hazard resulting from the messy Integrated Social Welfare Data. The data of aid recipients can be updated, validated, and monitored quickly and accurately based on proposals from regional governments. This means that the disbursement of the social protection funds which are worth Rp 242.01 trillion (US$16.69 billion) will not only be faster but also can reach the targeted recipients. Unfortunately, the government prefers eight social protection schemes with a variety of distribution formulas.

The disbursement of the funds for the National Economic Recovery program will be more effective if it is integrated into the financial system. The allocation of the National Economic Recovery funds for micro, small and medium enterprises (MSME) alone reaches Rp 123.46 trillion. Financing through digital-based financial services should accelerate the distribution of MSME financing. Moreover, the Mandiri Institute survey in August 2020 shows that around 43 percent of MSMEs have limited their business operations due to the shortage of capital.

On the other hand, data from the Cooperatives and Small and Medium Enterprises (SME) Ministry shows, until June 2020, only around eight million MSME players or 13 percent of the total could benefit from the digital technology. The National Economic Recovery Program for MSMEs can be integrated with application-based financial services, similar to peer-to-peer (P2P) online lending platform, while encouraging MSMEs to go digital.

The financial inclusion program should also be integrated into the National Economic Recovery program. The coverage of MSMEs will be wider and more accurate, especially with the distribution of assistance for productive micro-businesses through the subsidized people’s credit program (KUR) with zero percent interest.

Kompas

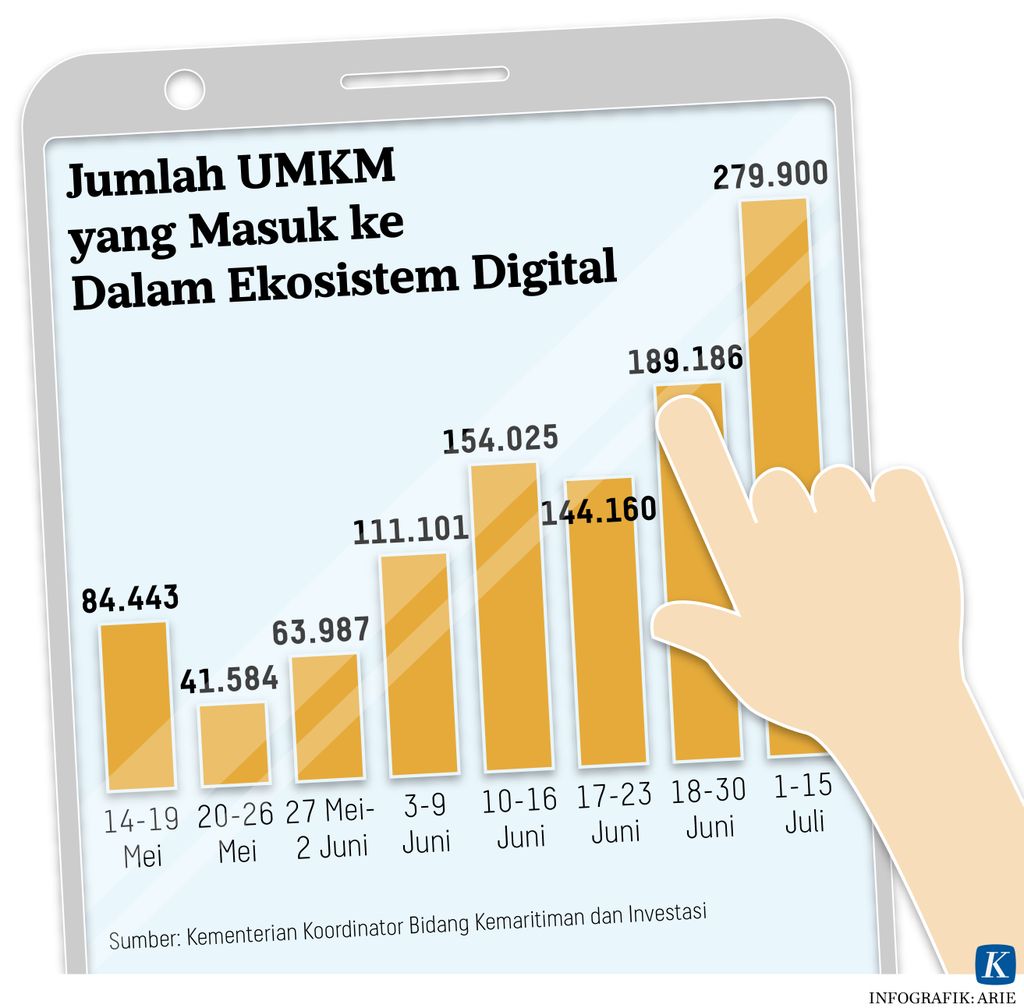

Number of MSMEs Included in the Digital Ecosystem

The KUR loans for ultra-micro businesses targets three million borrowers to specifically to support the productive activities conducted by housewives with a credit limit of around Rp 3 million. In addition, the loans are also given to workers who were dismissed with a credit limit of around Rp 10 million. The government has also allocated assistance of Rp 2.4 million for productive activities for up to 15 million MSMEs (with total credits of 22 trillion).

The budget allocation to mitigate the impact of the Covid-19 pandemic is quite abundant. Moreover, specifically for the social protection budget, the 2020 State Budget has set aside Rp 495 trillion.

This means that if those social protection programs are integrated, it should be more than enough to mitigate the impact of Covid-19 on all poor people (If included with those vulnerable to poverty affected by Covid-19) could reach between 40 million and 50 million people. At least with a rough and simple simulation, with a budget of Rp 495 trillion, each poor and vulnerable poor people can receive about Rp 10 million.

Likewise, if the economic stimulus budget allocation is effective and right on target, it should also be sufficient to sustain and restore various economic activities.

In fact, the economic activities until the third quarter of 2020 still suffered a contraction. The loan disbursement only rose 0.12 percent in August, and slightly higher at 1.04 percent in September 2020. Once again, the digital transformation should be further pushed to increase financial inclusion, which could in turn strengthen economic recovery efforts.

ENNY SRI HARTATI, Senior researcher at the Institute for Development of Economics and Finance (INDEF).